By Derek Horstmeyer

Many investors hold an S&P 500 index fund in their portfolios, thinking it is a low-risk way to keep pace with the market and a counterweight to other holdings like bonds and international stocks.

But most don’t realize that the index isn’t what it used to be—both in terms of what’s in it and how risky it is.

To assess the implications of the changes, my research assistants (Reema Hammad and Raheeg Joari) and I collected data on the S&P 500 over the past 50 years, examining how the components of the index have changed and thereby its interest-rate sensitivity, dividend yield, and volatility.

The main takeaway: The S&P 500 has become more highly concentrated in technology and financial stocks (and hence more sensitive to interest rates) and more correlated with other indexes around the world. This has implications for how investors can diversify their total stockholdings.

More tech, more financial

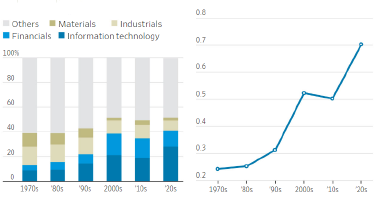

First, we explored how the composition of the S&P 500 has shifted over time. In the 1970s, industrials and materials made up 26% of the S&P 500, but this has decreased over time and now stands at just 10.6%.

Conversely, information tech and financials made up 13% of the S&P 500 in the 1970s before becoming the dominant sectors. Today, financials and information tech comprise 42% of the index by weight, with tech representing 29 percentage points of that figure.

In fact, six out of the top seven positions in the S&P 500 by weight are in the tech sector currently. This means that investors’ largest risk in holding the S&P 500 is the same as holding tech firms directly-interest-rate risk, lofty price valuations and heady growth-rate expectations.

More Correlated

The S&P 500 used to give investors a diversified bucket of stocks, but as technology and financial stocks have replaced industrials and materials in the index, it has become more correlated with global markets.

Next, turning to the stock-price metrics within the S&P 500, we have seen valuation levels increase since the 1970s. The average Shiller CAPE price-to-earnings ratio-which is an inflation-adjusted measure of a stock price divided by the average of 10 years of earnings-was 13.5 in the 1970s, and climbed to over 30 by the early 2020s. This highlights just how sensitive to interest rates the U.S. stock market is now.

Expectations for earnings growth are at a record high, and even a slight change in interest rates can derail valuations. Тo see this firsthand, investors need only to look to 2022, when the Federal Reserve raised rates by 5 percentage points and the S&P 500 went down 20% for the year.

In addition, the S&P 500’s dividend yield has decreased from 4.11% in the 1970s to 1.45% in the 2020s. Dividends lower the volatility of stocks for investors by mitigating losses, meaning that the S&P 500 has lost more than half of that portfolio bulwark over the past few decades.

Correlation with global indexes

Finally, we see a steady increase in correlation between the S&P 500 and the top 10 world stock-market indexes from Germany, the U.K., France, South Korea, Hong Kong, Japan, Toronto, China, Mexico and Brazil. In the 1970s, the average correlation between the S&P 500 and other global indexes was just 0.24-meaning returns in one part of the world didn’t often match those in another part. By the early 2020s, this correlation had jumped to 0.70.

This has implications for how an investor thinks about diversification in his or her stockholdings. In the 1970s, one could add a few world indexes to U.S. holdings and get a significant reduction in risk. But today, it no longer works that well to add Germany’s DAX or the U.K.’s FTSE to minimize the risk of a portfolio’s S&P 500 holdings-they are too highly correlated today to reduce overall portfolio volatility that much.

In all, the present-day S&P 500 is top-heavy on tech and highly correlated with other world indexes-with high sensitivity to rates and without the robust dividend yield of yore. This means that the 60-40 portfolio that worked in the 1970s to address diversification issues no longer works as well-and it will no longer work to just add international stocks for diversification purposes. If investors want the same diversification benefits they had years ago, they are going to have to be creative and include not just stocks and bonds, but also commodities, alternative assets and other uncorrelated, or weakly correlated, asset classes.

Derek Horstmeyer is a professor of finance at Costello College of Business, George Mason University, in Fairfax, Va. He can be reached at reports@wsj.com.

Source: https://www.wsj.com/finance/stocks/sp-500-tech-financial-stocks-weight-62ed530a